Outlook for Q-2 Manufacturing Rises Significantly: FICCI Manufacturing Survey

#Manufacturing #FICCI #Survey

● Higher percentage of Respondents report increased production

● Cost of Doing Business goes up - Higher Percentage of Respondents Report Rising Cost

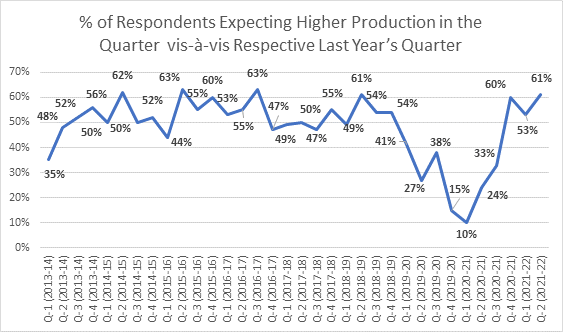

FICCI's latest quarterly survey (Q2) on Manufacturing reveals that after experiencing subdued Q-1 (April-June 2021-22), outlook seems to have improved significantly in Q-2 (July-September 2021-22). The percentage of respondents reporting higher production in second quarter of 2021-22 (July-September 2021-22) was much above the fifty percent mark- around 61%. This was significantly higher than the similar percentage of last year's Q-2 quarter (around 24%). This assessment is also reflective in order books as 72% of the respondents in July-September 2021-22 expected higher number of orders vis-a-vis April-June 2021-22.

Figure: % of Respondents Expecting Higher Production in the Quarter

vis-a-vis Respective Last Year's Quarter

Source FICCI Survey

Cost of Doing Business and Production

However, the survey noticed a high percentage of respondents experiencing rising cost of doing business and production. The cost of production as a percentage of sales for manufacturers in the survey has risen for 80% respondents in Q-1 2021-22. This is considerably higher than that reported in Q4 2020-21, where 72% respondents recorded increase in their production costs. Industry respondents have attributed the hike in productions costs primarily to high fixed costs, higher overhead costs for ensuring safety protocols, drastic reduction in volumes due to lockdown, lower capacity utilization, high freight charges and other logistic costs, increased cost of raw materials, power cost and high interest rates.

FICCI's latest quarterly survey assessed the sentiments of manufacturers for Q-2 (July-September 2021-22) for eleven major sectors namely automotive, capital goods, cement and ceramics, chemicals, fertilizers and pharmaceuticals, electronics & electricals, metal & metal products, paper products, textiles, textiles machinery, toys and miscellaneous. Responses have been drawn from over 300 manufacturing units from both large and SME segments with a combined annual turnover of over 2.7 lakh crore.

Capacity Addition & Utilization

* The overall capacity utilization in manufacturing was 72% in Q2 2021-22, which again reflects signs of recovery in manufacturing. The future investment outlook however remains that of cautious optimism, as 32% respondents reported plans for capacity additions for the next six months.

* As mentioned earlier, cost of doing business remains a cause for concern for the sector. High raw material prices, high cost of finance, uncertainty of demand, shortage of skilled labor and workinag capital, high logistics cost, low domestic and global demand due to imposition of lockdown across all countries to contain spread of coronavirus, excess capacities due to high volume of cheap imports into India, unstable market, high power tariff, are some of the major constraints which are affecting expansion plans of the respondents.

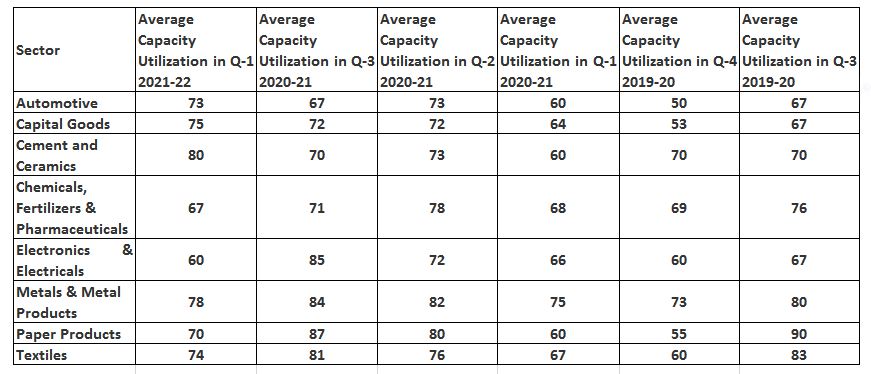

* The table below, gives average capacity utilization for Q1 2021-22 for various sub-sectors of manufacturing.

Table: Current Average Capacity Utilization Levels as Reported in Survey (%)

Inventories

* 85% of the respondents expect either more or same level of inventory in July-September 2021-22, which is higher as compared to the previous quarter, where around 79% respondents expected either more or same level of inventory in Q-1 2021-22

Exports

* The outlook for exports seems improving as around 58% of the participants are expecting a rise in their exports for Q-2 2021-22 and 30% are expecting exports to continue to be on same path as that of same quarter last year.

Hiring

* Hiring outlook for the sector remains subdued as 68% of the respondents mentioned that they are not likely to hire additional workforce in the next three months. This presents a near stable situation in the hiring scenario as compared to the previous quarter Q-1 of 2021-22, where 69% of the respondents maintained similar sentiments.

Interest Rate

* Average interest rate paid by the manufacturers has reduced slightly to 8.7% p.a. as against 9% p.a. during last quarter and the highest rate remains as high as 14%. The recent cuts in repo rate by RBI has not led to a consequential reduction in the lending rate as reported by 66% of the respondents.

Sectoral Growth

* Based on expectations in different sectors, some sectors are likely to register strong growth in Q-2 2021-22 except few as given in the table below.

Table: Growth expectations for Q-2 2021-22 compared with Q-2 2020-21

Note: Strong > 10%; 5% < Moderate < 10%; Low < 5%

Source: FICCI Survey

Back to Business Scenario in Manufacturing (Unlockdown period)

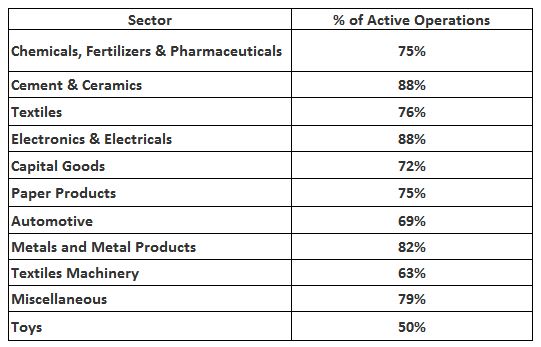

* As evident from the table below, some sectors like toys, textiles machinery are more affected in terms of ongoing operations in the factories as per the demand and current orders post easing out of lockdown restrictions.

Table: Operations taking place in facilities post easing of the Lockdown Restrictions

Workforce Availability

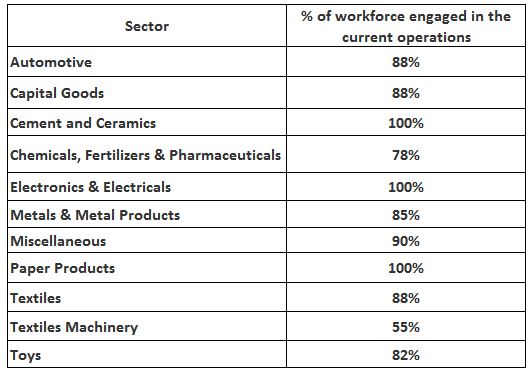

* Most sectors have sufficient labor force engaged in their operations and are not facing shortage of labor at factories.

Table: Workforce Engagement in Factories